The Forrester Wave for AI Consulting Services dropped for Q2 2026. Most readers will scan the quadrant, note which firms landed near the top, and move on.

The more useful signal is in the criteria.

What Forrester chose to measure, and reward, tells you where enterprise buying behaviour has actually moved. And the shift it reveals is significant, not just for AI consulting firms, but for every enterprise currently evaluating how to resource an AI programme.

The Criteria Are a Confession

Analyst firms build evaluation criteria by talking to buyers. The criteria that make it into a Wave reflect what those buyers are struggling with, prioritising, and demanding from the partners they hire.

So when the Q2 2026 Wave rewards firms specifically for operating model design, AI architecture, production deployment capability, value management, and governance in regulated environments, that is not abstract market commentary. It is buyer frustration showing up in the scorecard.

The market has moved past AI strategy theater.

What the Previous Phase Looked Like

A year ago, many enterprise AI engagements still centred on vision workshops, maturity assessments, and executive alignment sessions. Those deliverables were not useless. But too often, they became the entire engagement.

A polished AI strategy document would get handed to an internal team that lacked the architecture, data foundation, governance model, or organisational capacity to execute it. The programme would stall. The consulting firm would move on to the next engagement.

Buyers remember that. The Forrester criteria reflect the scar tissue.

The enterprise AI market now has a decade of accumulated pilot experience across most large organisations, and a pattern that is consistent across almost every sector: the strategy was fine. The gap between strategy and production is where the value disappeared.

"Enterprise organisations are not buying an AI strategy in 2026. They are not buying a framework or a maturity model. They are buying operational confidence."

Where the Frustration Now Sits

The pressure on enterprise AI programmes in 2026 is no longer about whether to invest. That debate is mostly over. The pressure is operational.

Enterprise buyers are asking a different set of questions from the ones they were asking 18 months ago.

Can this partner integrate AI into workflows our teams already use? Can the architecture survive our security review, data governance requirements, and compliance obligations? Can we measure value against a real baseline? Will anything still be running six months after the engagement closes?

That last question is the one that has changed the procurement conversation most sharply. AI programmes rarely fail during ideation. They fail in the transition from proof of concept to sustained production. That transition requires architecture decisions made early, governance built into the system from day one, and delivery accountability that extends beyond handoff.

Advisory-only firms are not structured to provide that. The Forrester criteria now explicitly penalise the gap.

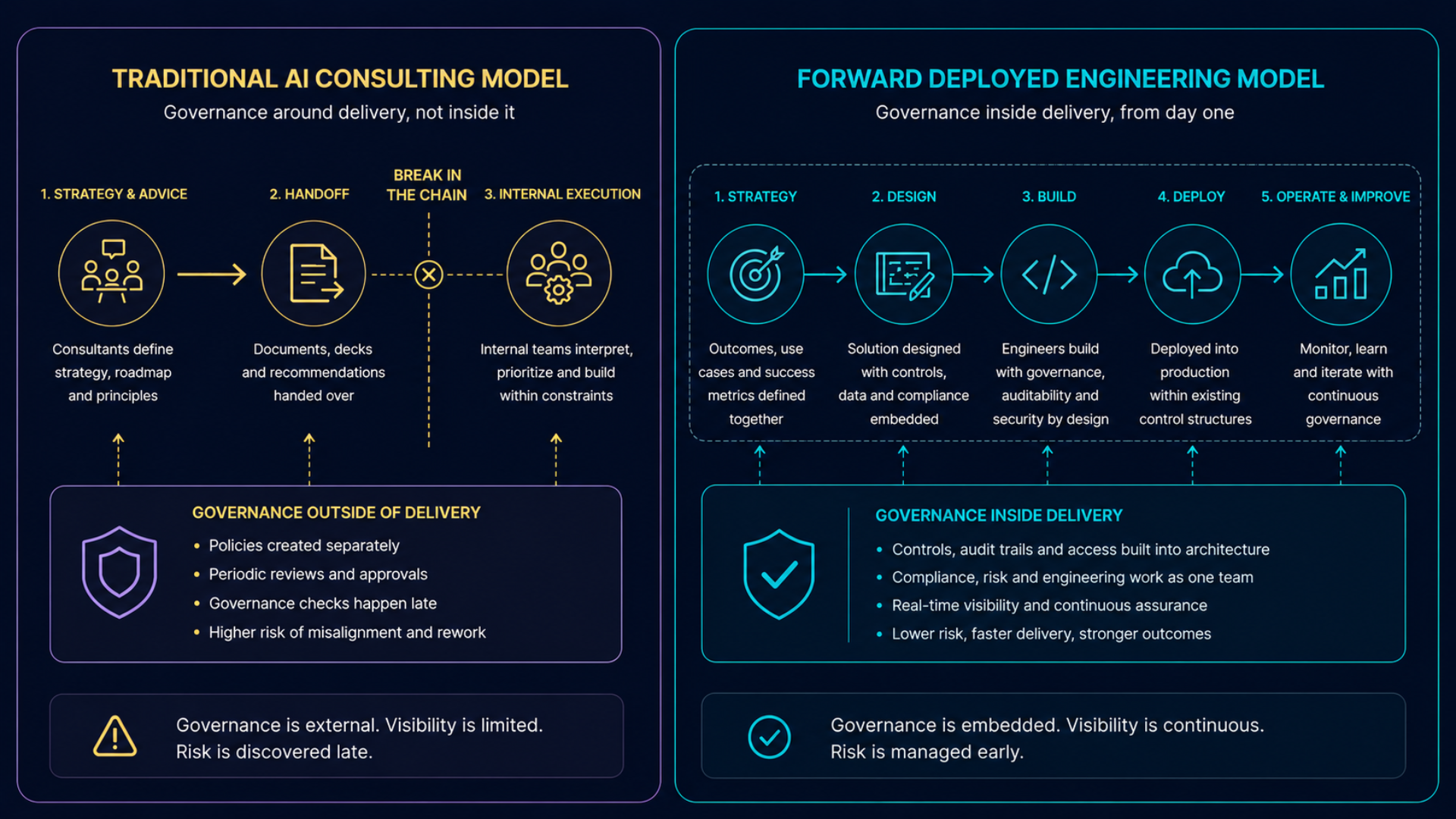

Governance Has Moved Inside Delivery

One of the clearest signals in the Wave is how governance is now treated.

For years, AI governance lived mostly as policy. It sat in risk, legal, or compliance functions, producing principles, review boards, and approval frameworks. Those things matter. But they were almost always disconnected from how AI was actually being built and deployed.

That separation no longer works, particularly in regulated industries.

In financial services, automotive, and industrial manufacturing, governance is now part of delivery, not a separate workstream that reviews delivery. Firms winning in these sectors can demonstrate they deploy AI inside existing control structures, with audit trails, explainability, and access controls built into the architecture from the start.

Inside the controls. Not around them.

That is a fundamentally different capability from strategy advisory. It requires engineers, compliance understanding, and business owners working together from the first day of the engagement, which is precisely the model that forward deployed engineering is built around.

Outcome-Based Pricing Is a Filter, Not a Feature

The Wave also surfaces outcome-based pricing as a differentiator among stronger performers, and it is worth understanding why.

When a delivery partner puts part of its fee at risk against measurable client outcomes, it is making two claims simultaneously. First, a claim about delivery confidence, that it expects to produce the result. Second, a claim about method maturity, that its execution patterns are repeatable and measurable enough to price against.

You cannot credibly price delivery risk if your engagement mostly ends at recommendations. You need defined milestones, measurable outcomes, and enough control over the actual delivery to influence the result.

This is why outcome-based pricing is a filter rather than just a commercial arrangement. It separates firms that have operationalised AI delivery from firms still selling advisory hours under AI branding.

The question every enterprise buyer should be asking any AI partner: which of your recent engagements had fees at risk? What were the outcome metrics? What happened when a target was missed?

Those answers are more diagnostic than any quadrant placement.

What This Means If You Are Evaluating an AI Partner

The Forrester Wave Q2 2026 is useful as a starting filter. It is not sufficient on its own. Analyst evaluations depend on the information firms provide and the references they nominate, which means a Wave reflects how well firms present their capabilities and how satisfied their nominated clients are. It will not show delivery failure rates, abandoned programmes, or the gap between what was sold and what was actually delivered.

The Wave tells you what the market is rewarding. It does not tell you which specific firms actually deliver against those criteria in practice.

The evaluation questions that matter most in 2026 are these:

Where will the engineers actually work?

A genuine delivery-capable partner embeds its engineers inside your environment for the duration of the programme, not at scheduled touchpoints from a remote delivery centre. The forward deployed engineering model is built specifically around this operating principle.

Where does accountability end?

A delivery-capable partner measures success at production adoption and business outcome, not at technical handoff. Ask explicitly what happens if the deployed system is not adopted by the teams it was built for.

Can they show governance built into architecture, not bolted on afterward?

This is the question that separates firms that understand enterprise AI governance from firms that have a governance slide in their deck.

What does their track record in your sector look like?

Automotive, FMEG, financial services, and industrial manufacturing each have specific integration constraints, compliance requirements, and organisational dynamics that generic AI delivery experience does not prepare a partner for.

The Shift in Plain Terms

The enterprise AI market in 2026 has moved through a predictable maturation cycle. The early phase was about awareness and exploration. The middle phase was about strategy and planning. The current phase is about delivery and production, and the gap between firms that can genuinely do that and firms that can convincingly describe doing that is wider than most buyers currently realise.

The Forrester Wave criteria are the clearest signal yet that the market knows this. The firms being rewarded are the ones that have closed that gap, not the ones with the best positioning language.

For enterprise leaders evaluating AI programmes, the practical implication is straightforward. The question is no longer "does this partner understand AI?" Almost everyone does. The question is "can this partner actually get AI into production in our environment, within our constraints, and stay accountable until it is genuinely running?"

That is the question the Forrester criteria are now built to answer. It should be the question your procurement process is built to answer too.

How Vishleshan AI Is Positioned Against This Shift

Vishleshan AI's forward deployed engineers work inside client environments across automotive, FMEG, financial services, and supply chain, embedded from day one, accountable through to production, and operating within the governance and integration constraints of the client's actual systems rather than around them.

The Vidura Agentic Platform provides the governance infrastructure, the Intelligent Gateway, the Context Manager, and the Governor, that allows AI to be deployed inside enterprise control structures rather than as a parallel system that compliance teams have to review after the fact.

This is the operating model. And it is the model the Forrester Q2 2026 criteria are now built to reward.

Vishleshan AI's forward deployed engineers take AI from use case to production in 90 days, inside your environment and within your governance constraints. Book a Consultation